At Sea At Peace

-

Posts

1,312 -

Joined

Content Type

Forums

Store

Blogs

Downloads

Events

Gallery

Everything posted by At Sea At Peace

-

Yep, 2 more months of the 'summer season' that they also do not expect to generate net income. And if the customer deposits are used during this period, the the Statement of Cash Flows will invert from such and possibly generate a NEG quarterly cash flow. "Bean counters" have been regularly disparaged. Unlike a CEO, they are generally credentialed financial professionals with a stronger mandate to "report the data" and are not usually in the "spin" business as is the CEO with "parse statement counseling" and one "dab of lipstick after another." He's not a true CFO, CPA bean counter. He hasn't been the CCL "bean counter" for the past 5-7 years; rather, the COO. Prior, he was Treasurer. Prior, he was Counsel. Given such, the lipstick will continue to be heavy and the statements well parsed.

-

Yep, I did. I can't find a Statement of Cash Flows for the Quarter? I can derive it however from the February Quarter NEG Cash Flow of $2.524B for 3-months then the May 6-month NEG Cash Flow of $1.888B would impute that the Quarter ended May 2022 would have been a POS of $636M. So, yep. Back to "Customer Deposits" counted as CF from "Operations." 3-months ending February, increase 187M. 6-months ending May, increase of $1.611B. So, of the $636M in POS cash flow for the quarter ending in May, $1.424B came from "Customer Deposit" OPERATIONS and the rest was NEG cash flow from Operations of $1.061B. Again, you were correct, and it might be semantics, but have POS cash flow for a quarter with otherwise $1.061B in NEG cash because of "increased Customer Deposits" of $1.424B just seem like a financial operating turnaround to me. 🙄

-

Well, the 10Q financial statements filed with the SEC, including the Statement of Cash Flows, indicate otherwise. https://www.sec.gov/ix?doc=/Archives/edgar/data/815097/000081509722000054/ccl-20220531.htm

-

Good question. Let's take a look. Yep, they have more debt as well as more cash. Also, as with the other two major public lines, their cash is primarily comprised of customer deposits. The above is from most recent 10Q or 10K. Below in pre-pandemic 2019 10K's.

-

https://www.sec.gov/ix?doc=/Archives/edgar/data/815097/000081509722000054/ccl-20220531.htm Well, there are two particularly interesting components to consider in "their statement" (which I believe they stated they achieved during the quarter), parsed as another member post in this thread so eloquently did, why not state "when?" The last week? 😉 https://www.cruiseindustrynews.com/cruise-news/27750-carnival-corporation-reports-q2-2022-earnings-business-update.html "Cash from operations turned positive in the second quarter of 2022." Note "in" not "for." 1. Cash Flow for the entire quarter was a negative $1.888 billion. As presented in the required components of the Statement of Cash Flows, Cash Flows Provided (Used) in Operations was a negative ("used") $1.209 billion, Investing Activities (Used) was a negative $3.107 billion and Financing Activities (Provided) positive $2.463 billion (and an Exchange Rate Decrease of $0.35 billion). 2. Cash Flow for the quarter, adjusted with a financial perspective of Customer Deposits classified as "short term deb" aka an "interest free" Customer Line of Credit (as some believe it is; collecting Customer Deposits is a tough sell at this point as from Operations), the Operating negative cash flow would have been $2.820 billion.

-

Really good to look at and parse the quotes. 👍 These CEO's and management have become POLS in their selective grammar are true to form inventive and creative word salads. Great discussions. Wouldn't it be nice to get an honest answer to the real question since the earnings release? The real question being "how did you still lose almost $4B with current operating revenues of $4B on 6-month YTD when you lost $4B in the prior comparative period on operating revenues of $75M (million). Once that is answered without preferential parsing, a follow up with "how are you going to make corporate Net Income in the current summer quarter to end August 30th and, yikes, in the historically weakest quarter to follow ending November 30th?"

-

Well, IANAL, but follow the progression of what happens "on the way down." Stock values generally aren't causal to bankruptcy though they can indicate the markets determination that such might be in the offing. The first bankruptcy threshold they face are likely embodied in the "covenants" on their debt and leases; such as performance, financial ratios, liquidity levels, etc. spelled out in their debt agreements and the inability of the company to "strike a new or modified deal" when they have "fallen out of covenant compliance." Less likely is an unpaid vendor aka Crystal ships seized for unpaid fuel bills (which was pretty rare) setting off other events faster like dominoes. In the meantime, for the stockholder to watch when share prices that drop fast and get below the $5 and $1 per share thresholds. That triggers "a bunch of potentials." Institutions, pensions, mutual funds, etc. may have provisions whereby they are self-limited from investing (owning stock) in such companies. It's a double whammy potential in that as the $5 threshold approaches and actually hits, those with such restrictions could force a VOLUME SELLOFF to meet their own requirements which can magnify the price drop. Also, listed on the NYSE, the is a 30-day rolling average measurement of under $1 RISKS DELISTING from the NYSE. A company could then move over to the OTC markets (pink sheets). Again, IMO, IANAL. 😉

-

Three very good points.

-

Unlike more traditional public companies and debt structures, the cruise lines debt structures are a complex web and tiered secured, unsecured senior and unsecured (general), as well as vendors (fuel contracts, etc.) and the massive, generally unsecured, customer deposits. The debt "web and tiers" vary, some with first secured priority on a ship, group of ships, a private island, and other senior unsecured priority not on a specific asset but on on all other assets. The "company" doesn't control what happens. The creditors do, and almost universally and historically, the creditors are their to protect the most senior creditors only. Equity would be gone, with no apparent reality for an aka Equity Committee as their is no prognosis that there is residual assets net of debt and creditor settlement. Where the "mess" comes in is where the creditors line up, by ship, group of ships, private islands, etc., the all other assets. They have unique, secured positions that prevent other creditors from touching "their secured ship, group of ships, private islands, etc.). What is NOT CLEAR, but subject to dire outlook, is who (if anyone) will honor customer deposits? The "corporate entity" owns the customer deposits. The debt, secured as described above, has no claim to such (let's just say) for their ships or groups of ships (possibly by subsidiary line, however). Possibility for some of the most convoluted bankruptcies and/or liquidations since we've seen during the 2008-2010 timeline. The most notable, messy bankruptcies also got "first dibs" on billions of professional fees (ahead of creditors).

-

Yep, that is out there. I've always like the 110% award trophies, especially the ones given out by the coach to his son or daughter. 😄 Yes, the are projecting 110% capacity for their 3rd quarter (3-months ending August 31st). That is their "summer season." The need to make a boatload of net income to make it through the 4th quarter and restart a new year December 1st) However, they are also projecting a NET LOSS for the (greatest 110% on all ships) 3rd quarter. https://www.marketwatch.com/story/carnival-now-expects-3q-loss-positive-adjusted-ebitda-271656078653#:~:text=Carnival%2C the world's largest cruise,expected to end Aug. 31. Be not concerned, they'll deflect to the new talking point (i.e., lipstick) to a new measurement level that we should look to ~ EBITDA should be positive. LOL. In essence, we won't make money during this massive summer cruise season with 110% capacity "unless we don't count Interest, Taxes, Depreciation and Amortization." 🤥 Try that yourself at the bank. 🤣 Further, per their recent earnings release, they give ZIP, NADA, ZERO indications for the 4th quarter (3-months ending November 30th; not an overwhelmingly optimistic date range for the travel industry and especially cruise lines). The "tipping point" possibly ahead of continued loss earnings reports is a decrease in historical demand, a reduction in cruise bookings (out of cautions) and erosion of their free Line of Credit; i.e., customer deposits. Reported "liquidity" is $7.5 billion. Comprised of the component "customer deposits" of $5.1 billion.

-

YIKES! Been out this morning prepping for the 4th. FYI, previously posted (somewhere) the NCLH March "low" adjusted for additions common shares issued and outstanding is (if I recall) $3.60 per share. Got a ways to go. CCL's investors earnings release was brutal fact set for all cruise lines, despite the cruise lines continued lipsticking of bookings are up (what month, what year, etc.), on board spending is up and the ships are all back. FACT of the matter, year over year, their revenues were $4 billion higher than the $75M prior, and their losses were still almost $4 billion. 🙃

-

Just wanted to support such previous statement that "debt" is a better weighted indicator of what's going on. The CCL debt issuance, depending on features, are dropping since the beginning of the year; some by 40%+- (raising the imputed "yield" to junk bond status). Pretty much the same general message from RCL's.

-

CCL's earning release was very pathetic based on fundamentals. Unfortunately, the stock market, especially traders, make money on volatility in the short run and could care less about such basics. [As a side note, CCL, RCL and NCLH "debt" has fallen off the table since 12/31/2021 "massively" and CCL "debt" has moved from much smaller than "stockholder's equity" to overwhelming it proportionally. So, the drop in the valuations of debt speak through a louder megaphone than equity stock PPS changes.] Back to the CCL earning release, YIKES (yes, I am screaming). 😉 Here is copy of a post in another stock thread. CCL (and RCL and NCLH) management and governing boards have to stop using the "bookings are good" and "on board spending is up" and "the number of our cruise ships back in service is..." LIPSTICK. Seriously read the below, especially the last line. It is stunning (fundamentally). https://www.sec.gov/Archives/edgar/data/815097/000081509722000044/a20222qbusinessupdate8-k.htm

-

Yep. Also noted an article today. Usually take such with a GOS, but did verify the debt data and did a little 'what's the impact chart. Here's the imputed debt load currently per 2019 pre-pandemic passengers; the average being $3,640. I was surprised. https://www.fool.com/investing/2022/06/27/why-cruise-line-stocks-dropped-today/

-

Have had a bit more time taking a look at them as a reference for RCL and NCLH. It is stunning what lipstick can't do. Hopefully RCL and NCL won't have this "success" level when they next report. 😲 They boast* liquidity of $7.5 billion. 🤥 * which includes $5.1 billion (or 68%) in customer deposits. They boast* about revenues, occupancy and cruise capacity. 🤥 * so, let's take a look at how operating at such "peak performance" has affected the bottom line. Revenues - Passenger ticket and Onboard and other $4.024 billion 6-months ended 5/31/2022; Net Loss $3.726 billion. Revenues - Passenger ticket and Onboard and other $75 million 6-months ended 5/31/2021; Net Loss $4.045 billion. They increased revenues by $3.949 billion, or 52.5X (times) or 5,265% in order to reduce their comparative loss $319 million; i.e., they only improved (less loss) generating $4.024 billion in revenues compared to just $75 million.

-

Yep. There are a lot of bond issuances by the big three, with a complex web of collateral (direct or indirect). We're big, pro-cruising and believe beautiful ships will always sail. However, the cruise industry (all including the big 3 publics) had an enormous rise in passengers pre-pandemic for a decade. Accordingly, they all added ships, ordered newer ships, ordered newer powered ships, expanded private islands and port assistance projects. So, post-pandemic, how long will it take for the linear projection of the passenger growth that was expected and the basis for the tens of billions of pre-pandemic expansions (above), to get to the level that can (1) support the capacity they expected and (2) recoup a level of profitability to get the debt to equity ratio back to where it was during their extremely profitable years? My focus on debt is the belief that the real money (the debt holders) has already realized that such isn't going to be happening soon; hence the significant drop in debt trade values to face and related leaps of yields (effective interest rates derived). Traders can and do make a lot of money on volatility and the prices declines and 'dead cat bounces' on the continued reporting of "losses of billions aren't that bad" and "future bookings are bright." They will have a good 2022 summer, and need it. However, unlike restaurants and attractions in the northern states (lakes, oceans, etc.) that work to make enough during their summer 8-10 premium weeks to pay the bills upon closing after the season to get to the next year, cruise lines can't just turn off the power and lock the doors for the late Fall, Winter and Spring (and survive on a November holiday, a year end holiday week and a spring break). Oh well, thanks for taking the time to look at the focus of the issue.

-

Yep, but less worse than previous anticipated is a 'traders celebration for sure. 🙄 Oh why look at the hard data. Losing almost $2B in the quarter is GOOD NEWS. 😄😂 As they sing at Fenway Park, "so good, so good, so good." Lots of trades today 'short. 😲 On a major UP day. The debt issuances didn't increase today as the equity. Hummm.

-

Yep. 4 sure. Take care. 👍

-

Well, since both are hypotheticals steeped in confirmation bias, i.e., an imaginary scenario, then sure. I don't know how you can actually predict that you can buy RCL at $25 or equally that RCL will actually rise to $55. But hey, the experts can't either. The core of the post (not substantively debated or discussed in the one liners) was that looking at the "debt-side" price and yield changes in just the past 6 months and the relative size of "debt to equity" (either stockholder's equity or MKT CAP), and that change since pre-pandemic, highlights that "debt" is massively more weighted than equity (a big change from pre-pandemic) and information about the changes in the values (sales, trades data) give more appropriate reference to analysis of the financial investors in the market. The "debt market" has totally upended the "equity market" in valuation (see BELOW). Again, the point was that the debt market has been very, very negative in the past six months (citing one as an example).

-

That's probably why I indicated that "IMO the best financially prepared of the big 3" and did not proffer such as a guarantee of future success. 😉 Also, such presentation was focused on the debt value (price) declines in 5 1/2 months, indicative of significantly increase risk assessment (of the financial experts in the OP in response quote) and supposition that such on debt is likely a better indicator than a focus on equity. Of further note, the MKT CAP of the big three (i.e., equity valuation) is but a fragment of both their historical amounts and in relation to their current debt load (i.e., following debt is heavily weighted). 🤨

-

IMO, we are past the point of looking at equity (i.e., stock PPS) as the indicator of what financial experts think. Taking a look at the debt since 12/31/2021 to today 6/22/2022 there is a stunning reduction in bond prices from face (inversely an increase in the yield over stated rates). Here is one of RCL's bonds as an example of the above. Again, looking to the debt, which is the first in line at the creditors table, speaks volumes in the confidence level in RCL (IMO the best financially prepared of the big 3).

-

The ultimate compliment accepted. 😉 The post of the historical performance of an OP referenced Wells Fargo advisor was totally fact-based. Not trying to sound logical in presenting hard, cold facts; i.e., nothing personally imparted. Simply raw data. Like some more on such? In 2021 the same WF team advised the 'tips' that follow. It's raw data, so please don't infer an attempt to sound knowledgeable. https://www.yahoo.com/video/wells-fargo-predicts-over-40-014307515.html

-

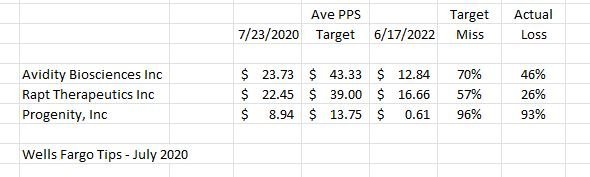

There clearly isn't a standard for who to trust as investment advisors. If you look at some of the names in the articles that are referenced in such posts, go back and look at the track record since the pandemic, you get a more informed basis for assessing whether you would follow such guidance "with your own money." Note, a lot of these 'experts' are not using their own money, it's all OPM, and most have moved to a % of assets / investments under management and not % performance. 🧐 However, although not taking stock advice from a social media platform aka CC, and being long-term cruisers, we can get valuable feedback on the performance of the cruise lines, passenger counts, service quality, pricing, satisfaction, etc. that assists in the financial considerations (fundamentals in the old days) for each. 😉 So, here's a look at a Wells Fargo July 2020 participated endorsement (including reference of the contributor to the above current list) of three particular stocks. I believe the link gives a "single look" before the paywall. https://www.tipranks.com/news/article/wells-fargo-these-3-strong-buy-stocks-are-must-watch-names/

-

It's good speculation that NCL would be a fit compared to others if MSC has such an appetite and inclination at all. NCL doesn't have and wouldn't need to continue spend on developing foreign markets that MSC focuses on and vice-versa. NCL also has the HAVEN concept akin to the MSC Yacht Club concept. They are a match in a lot of ways. Re: the 'pennies on the dollar, yep. Nothing for equity and a haircut for debt holders. CCL simply too big and completely different consumer. RCL, not sure if also too much to take on with overlap in geographic current markets.

-

Well, the CEO's have exhausted the "future bookings are back to normal or better" mantra (now indications are that discounting will be predominant to get passengers into next year) as well as this summer season looking great (also discounted late is reported). Heavy late discounting is taking place to add passengers to ships, FCC's are being used up, so late bookings will eat into the free cash flow line-of-credit from customer deposits. Really through no fault of their own, cruise lines have just been hit with one rogue wave after another, too long now to list, and restored capacities and new ships ahead, the supply (and cost) simply exceeds the demand (and willing to pay price). Pricing now is updated for the ridiculous increase in airfare and, in some cases, port area hotels trying to make back losses in a narrower time period. The ships, especially the newer ones, will still sail, it just doesn't appear under the current public ownership structure for the big 3. It is not reasonable to expect a vulture buyer or group to pay anything at all to shareholders and further likely to ask the debt holders for either huge interest rate and payment rescheduling concessions or significantly reduced negotiated payoffs. MSC is not buying any of these lines and has their own ship development plans as well as vertical expansion plans for shipping. They are however, flush with cash and capital, expanding on a SPREE ~ ~ their control of ports, buying Bollore Groups African ports for container terminals (47 African countries, 16 container terminals) for $6.4B and planning to buy, in a cash deal, Global Ports Holding, the worlds largest cruise port operator (26 ports, 14 countries) and 5,400 port calls in the Mediterranean, Europe, Caribbean and Asia. ~ their control of transportation, they also acquired the Torrejon railway and terminal in Spain for its Medway transportation hub from Spain to the Iberian peninsula and ~ more shipping strength, the Brazilian shipping freight transportation company (2/3rds) Log-In Logistica. ~ as a hedge to shipping backlog, they joined Lufthansa in making a joint bid for Italian ITA Airways for its cargo and passenger capabilities.